Q. What is APR and will it make loans cheaper?

Q. What do I do when I am not given this information by my bank or if am charged more than was initially in the APR?

This information is the right of every bank customer. Customers should raise any issues with the relevant customer care representatives or the banks’ head office. Customers can also email consumerguide@kba.co.ke and a Kenya Bankers Association member of staff will facilitate a response from the bank.

Q. Can I calculate the APR for myself?

Yes. Every bank customer can access the Total Cost of Credit template and APR calculator on the KBA website at www.kba.co.ke. The customer will still need to ascertain the accuracy of the costs from the bank so as to ensure that the self-computed APR is accurate. However, the APR calculator will provide a good indication of what to expect.

Q. Is this different from the bank’s base lending rate?

Q. Is APR the only basis of comparing cost of credit from different banks?

Q. Which other initiatives are banks working on to address high interest rates?

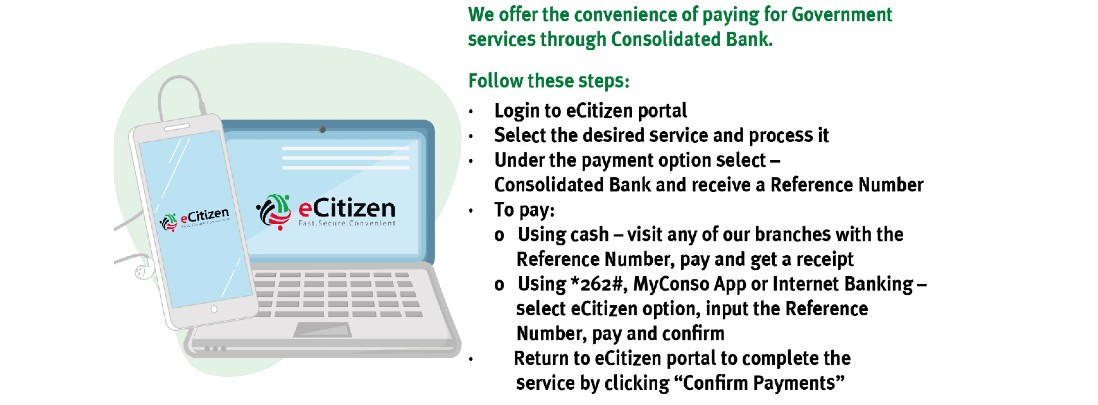

Q. What is iTax

(Integrated Tax Management system) iTax is a system that enables taxpayers to file returns electronically, make payments and enquire about their tax status online.

Q. How do I pay taxes using the iTax system?

Q. What is an e-slip?

An e-slip is an electronic ticket that contains the taxpayer’s details i.e. name, PIN number, amount of tax due.

Q. For how long is an e-slip valid?

An e-slip is valid for seven (7) days from the moment it has been generated from the KRA website.

Q. What if the e-slip is invalid?

If the e-slip is found to be invalid the customer has to go back to KRA website for another e-slip.

Q. What are the modes of paying taxes under the iTax system?

Cash (This is applicable to both CBKL and non-CBKL customers) For Consolidated Bank Customers one can use their cheque but their A/Cs must be funded

Q. What does the customer get after paying tax at Consolidated Bank?

The customer is provided with a receipt print out indicating that the taxes have been paid.

Q. What are the charges for using iTax?

CBKL will not charge for paying taxes under the iTax system.

Q. What types of taxes are payable under iTax?

All domestics taxes are payable under the iTax system.

Q. How long does it take for me to receive my cheque book once I place the order?

It takes 4 working days from the day you make the application to when you receive the cheque book.

Q. How long does it take for me to receive my ATM card and pin?

It takes 7 working days for the ATM card to be ready whereas the pin is sent to your mobile phone.

Q. What should I do upon the expiry of my ATM card?

All you need to do is visit any branch and your new card will be issued to you. In addition, you can visit any branch a month before expiry to renew the card.

Q. What should I do incase my ATM card is lost or stolen?

You should report the card stolen/lost by calling our toll free number 0800720039 or 0703016016 or WhatsApp 0729111637 for the card to be stopped. You will then visit any of our branches for instant issuance of a new card.

Q. What should I do if I forget the password of my ATM card?

For Chip & PIN card, we do not re issue another PIN. Instead you have to request and pay for another card.

The same case applies when a card is swallowed/stuck in another Bank’s ATM.

Q. What should I do if I want to increase the ATM withdrawal limit on my card?

Visit any branch and fill in a form indicating the new amount. The current limit is KES 40,000.

Q. What should I do if am interested in opening an account or applying for a loan and cannot visit the branch?

You can call the branch nearest to you and have them send the Direct Sales Team to assist you with the process.

Q. Does the Bank offer Mobile Banking Services?

Yes, it does. Please see more details under ‘E-Banking’

Q. What do you need to transfer money abroad?

The swift code of the Bank and the recipient's account details. The Bank’s swift code is CONKKENA.

Q. Does the bank undertake CSR activities?

Yes it does. Please see more details under ‘CSR’

Q. Does the bank offer mobile/ phone banking services?

Yes it does. Please see more details under ‘E cell banking’

Q. Does the bank offer trade finance facilities?

Yes, it does. Please see more details under ‘Trade Finance facilities’

Q. Does the bank provide LPO financing?

Yes, it does. Please see more details under ‘Solid Loop’

When you get your paycheck, take a percentage -- between 10 percent and 30 percent -- and put that away. You'll be rich enough to be financially independent within a short period of time.

Consolidated Bank is regulated by The Central Bank of Kenya.

Consolidated Bank is regulated by The Central Bank of Kenya.